Food Borne Illness Insurance

Restaurant Recovery

Key Features of the TNR® Policy :

- 24 Month Policy or Long Term Agreement Endorsement (2 year) available for qualified risks

- Alleged contamination versus proof of actual contamination (included in Definition)

- No sub-limits for adverse publicity from actual, suspected, or alleged food borne, restaurant, or supplier event incidents

- “Suspected or alleged” contamination coverage up to the applicable Restaurant or Supplier Event limit under the Public Announcement policy trigger

- Food Borne Illness includes actual or alleged illness suffered by customers and/or employees

- Supplier Event Incident includes occurrences when there is no formal recall

- Rehabilitation marketing costs provided

- Inoculations, Vaccinations, and Testing Expenses outside the limits

- 24 Month Policy or Long Term Agreement Endorsement (2 year) available for qualified risks

- Alleged contamination versus proof of actual contamination (included in Definition)

- No sub-limits for adverse publicity from actual, suspected, or alleged food borne, restaurant, or supplier event incidents

- “Suspected or alleged” contamination coverage up to the applicable Restaurant or Supplier Event limit under the Public Announcement policy trigger

- Food Borne Illness includes actual or alleged illness suffered by customers and/or employees

- Supplier Event Incident includes occurrences when there is no formal recall

- Rehabilitation marketing costs provided

- Inoculations, Vaccinations, and Testing Expenses outside the limits

Crisis Management Benefits along with purchase TNR® Policy:

- Unlimited Pre Incident Loss Control Assistance – Crisis Management consultants via email/telephone versus 10% of gross written premium limitation or other sub-limit

- Crisis Management Expenses does not require closure of the restaurant or a separate contract with the crisis management consultants

- Extra Crisis Management Expenses up to $300K for an event later determined to be an uninsured event/incident

- Unlimited Pre Incident Loss Control Assistance - Crisis Management consultants via email/telephone versus 10% of gross written premium limitation or other sub-limit

- Crisis Management Expenses does not require closure of the restaurant or a separate contract with the crisis management consultants.

- Extra Crisis Management Expenses up to $300K for an event later determined to be an uninsured event/incident

The policy and endorsements should be read in its entirety for all terms, conditions, limitations and exclusions that apply.

Learn TNR Insurance in 2 Minutes

Interested in our 30 minute TNR® slide presentation?

Interested in our TNR® Infographic?

Is Your Client's Company at Risk?

Any entity serving food, from restaurants to hospitality industries to cafeterias to food trucks, are at risk. They are held to a higher standard of care by the health departments and face unique exposures that other businesses do not due to their daily handling and serving of food to the public. Whether it’s actual or alleged, having one of these food borne illnesses within the settings can have a negative impact by decreased customers, revenues and reputation.

Trade Name Restoration – Longest Running Food Borne Illness Business Interruption Insurance Since 1998.

Highest Available Market Capacity of $120,000,000 per Trade Name!

Eligible Industries: Hospitality including Restaurants, Hotels, Movie Theaters, Bowling Alleys, Casinos, & more.

Underwritten by certain underwriters at Lloyd’s.

What is Trade Name Restoration (TNR®)?

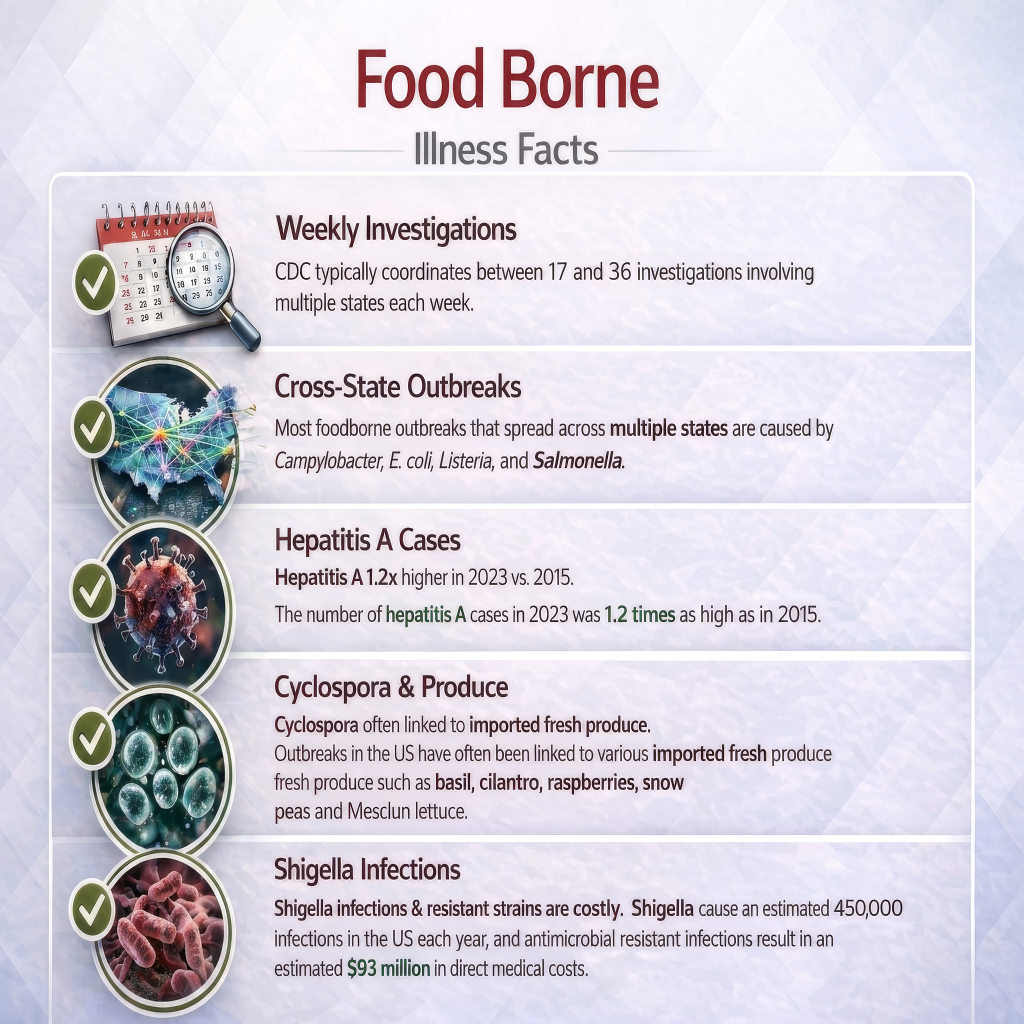

TNR® is the brand name of an insurance product pioneered by PLIS in 1998. This insurance provides restaurants & hospitality industries reimbursement of loss of business income and extra expenses that are incurred by the establishment, following an accidental or malicious contamination or food borne illness, such as Hepatitis A, E. coli, Salmonella, Shigella, Norovirus, Listeria, etc. These are considered to be food borne illness pathogens, which when transmitted through food and consumed, can cause people to become ill.

For more information refer to our TNR® Brochure

Trade Name Restoration (TNR®)

Restaurants/Hospitality Industries need extensive coverage.

Most service industry businesses serving food and beverage insure for customer injuries or lawsuits such as slips and falls. However, they may unknowingly leave their REVENUES exposed to the possibility of a food-borne illness outbreak.

What Does Our Policy Respond To?

Food Borne Illness Outbreaks:

- Accidental or Malicious

- Food Borne Contaminations (whether chemical, physical, or biological)

- Supplier Caused Outbreaks

- Suspected/Alleged Food Borne Illness Outbreak Accusations

- Trade Name Trigger (if an Insured’s location(s) operates under the same trade name as an uninsured location that experiences a foodborne illness event, & revenues at the Insured’s location are affected because of it, coverage will respond.)

- Extortion Event (Malicious Contamination Threat) (threat made by a third party to commit a Malicious Contamination)

- Accidental or Malicious

- Food Borne Contaminations (whether chemical, physical, or biological)

- Supplier Caused Outbreaks

- Suspected/Alleged Food Borne Illness Outbreak Accusations

- Trade Name Trigger (if an Insured's location(s) operates under the same trade name as an uninsured location that experiences a foodborne illness event, & revenues at the Insured's location are affected because of it, coverage will respond.)

- Extortion Event (Malicious Contamination Threat) (threat made by a third party to commit a Malicious Contamination)

Exposures

Restaurants/Hospitality Industries have risks specific to food that other businesses do not:

- Hepatitis A

- E. Coli

- Salmonella

- Shigella

- Norovirus

- Listeria

- And Even More...

See Food Borne Illness Events!

A single food borne outbreak for 250 people “could cost a restaurant millions of dollars in lost revenue, fines, lawsuits, legal fees, insurance premium increases, inspection costs and staff retraining, a new study from researchers at the Johns Hopkins Bloomberg School of Public Health* suggests.”

*NOT all costs are covered under the TNR®

policy

2. Salmonella Outbreak Linked to Cucumbers

3. Listeria monocytogenes Outbreak Linked to Ready-to-Eat

Sandwiches and Snack Items

Program Administrator for Lloyds Coverholder - Certain Underwriters at Lloyds

Insureds Have Exclusive Access To

Specialty Risk Management® , Inc. (SRM®).

SRM’s Crisis Team is crucial to the Insured’s survival before, during, and after an outbreak to respond to unfolding events and to rebuild your client’s brand & revenue.

Since 1997, SRM has had over a 95% Success Rate over the history of the company in controlling food-borne illness events BEFORE they become media events. If you never hear about our customers, we’ve been a success.

Highlights of SRM Benefits:

- 24/7 - 365 Days Crisis hotline for the Insured

- A closely integrated team with specific expertise and targeted response in the areas of Food Law, Public Health Law, Communicable Disease/Pathology, Media, Marketing Response, Customer Response, Business Recovery, etc.

- Toll-free customer helpline/outbreak response

- On-going support throughout the year for questions, projects, building reflexes, prevention actions, and early warning signs for quicker and more effective response to foodborne illness events

- And More...

© Copyright SRM® , Inc. and its licensors. All Rights Reserved.

This page is not intended to be a representation of coverage. See policy wording for details. All coverage

features are still subject to individual underwriting and certain coverage features may be restricted.